Drug prices

Finally! Humira’s biosimilars also hit the us market!

Humira was first marketed in 2002 and was protected in the US market until 2023, thanks to AbbVie’s use of two strategies :

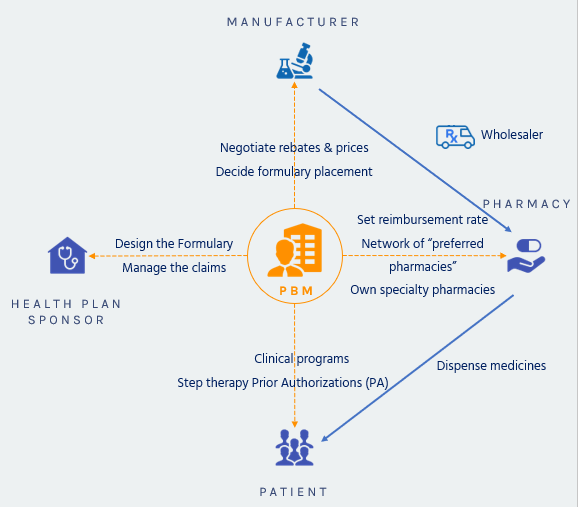

Negotiating Rebates from Drug Manufacturers

Manufacturers are supposed to provide a rebate if their product is preferred and put on the plan formulary, rather than a competitor’s product.

Negotiating Discounts from Pharmacies

Negotiating Discounts from Pharmacies

The same market competition mechanism is used with retail pharmacies: they will provide discounts to be included in a plan’s pharmacy network.

Offering More Affordable Pharmacy Channels

Offering More Affordable Pharmacy Channels

The PBM will promote mail-order services which generate savings on the dispensing costs, and build preferred pharmacy networks

Encouraging the Use of Generics and Affordable Brands

Encouraging the Use of Generics and Affordable Brands

Once a medication has lost its patent protection, competitors will launch “me-too” products or generics which are much cheaper than patent protected drugs.

PBMs design tiered formularies dividing drugs into groups based mostly on cost. A plan’s formulary might have three, four or even five tiers. Each plan decides which drugs on its formulary go into which tiers. In general, the lowest-tier drugs include the lowest cost generic drugs, and the highest the most expensive non-preferred brand specialty drugs. The lower the tier the lower the member’s copay.

Reducing Waste and Improving Adherence

Reducing Waste and Improving Adherence

Using formularies and tiered cost sharing, prior authorization and step-therapy protocols, consumer education, and physician outreach, PBMs try to lower plan costs.

Managing High-Cost Specialty Medications

Managing High-Cost Specialty Medications

Specialty pharmacies are another crucial tool to provide effective patient education, monitoring, and support for patients with complex conditions, such as hepatitis C, multiple sclerosis, or cancer.

Humira was first marketed in 2002 and was protected in the US market until 2023, thanks to AbbVie’s use of two strategies :

After wrapping up the 2023 enrollment, employers are now planning their next moves to mitigate the continuously growing healthcare costs impacting their plans. This is particularly true for pharmacy costs.

PhRMA, a Big Pharma lobbying group, released an advertising touting that drug prices were not fueling inflation. To prove it, they produce the graphic below.